To make the mainstream banking services available to all, RBI and government have been outlining many initiatives that could accelerate efforts on this. The year 2005 and 2006 witnessed two key initiatives of RBI to reinforce the financial inclusion drive by introducing ‘no-frills’ account and ‘business correspondent model’ of banking respectively. Since the inception of BC model, a large number of organizations have begun working as BCs for many banks and thus offering ‘no-frills’ account to prospect clientele through their network.

However, while these organizations have been experiencing business growth in terms of client outreach and number of transactions, many are struggling to remain financially viable. Furthermore, BC’s appointed Customer Service Providers (CSPs) – the most important pillar of the model crucial to its success, are also struggling to meet costs and maintain business viability. As of now, only a few experiments have been undertaken to explore the feasibility of the model and to understand clients’ perspective.

This article tries to summarise insights on certain crucial issues and challenges faced by the BC model, specifically CSPs and clients, from the recently concluded CMF’s research study on the BC model. The study was a two stage process in terms of analysis – first, it looked at the crucial aspects of cost and revenue pattern of customer service providers of BCs and second, it focused on issues related to CSP and client behaviour in order to critically assess the feasibility of the model.

Customer Service Providers are responsible for direct interaction with clients and to take the BC services to clients on the ground. A stratified random sample of CSPs (67) was surveyed and they were stratified according to location (rural 78% and urban 22%) and operations/services handled by them (no-frills accounts- regular transactions or remittances or disbursement of government aids and loan repayments).

CSPs selection and their business: Education, location and reference of other local agencies like police, panchayat, and banks are three key criteria that have been used by BCs in recruiting their CSPs. Close to half of rural CSPs (40%) surveyed, consider BC business as their primary activity as opposed to only 27% of urban CSPs. The data collected on their daily BC business transaction shows that on average, CSPs undertake 31 transactions per day. While, numbers of transactions is much higher (53) in urban centres (as remittance-heavy areas) whereas, rural centres struggle to meet even half the mark (23 transactions per day).

CSPs are of the view that the number of transactions can be increased if the BC channel could offer more client centric products and services (35%), can do effective marketing and promotion of the model (33%), lowering the charges (23%) and flexibilty in transaction limit (18%).

CSPs commission and Finances: CSPs are struggling to make their business profitable and financially sustainable as the current commission structure is inadequate to cover their operation costs. This situation is further exacerbated by reported low usage of ‘no frills’ accounts (NFAs) by clients (median- 2 transactions in last 3 months) and about 36% the sample did no transactions in last 3 months.

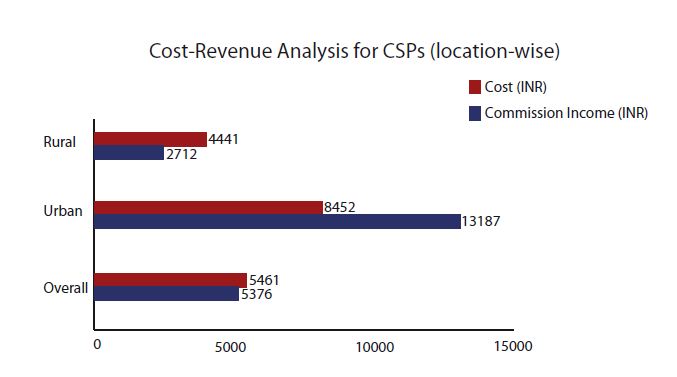

To establish a better understanding on the financial viability of the BC business, monthly recurring cost on different heads and monthly recurring revenue data were collected in BC business operation-area/location wise. Finally, the average figures are taken into account to understand the current financial viability of CSP operation. The below figure present the monthly cost and revenue of CSPs.

The above figure shows that on average, the cost incurred is higher than the income earned from commissions, however, the results are very different when one compares the alterations in rural and urban operations. For rural CSPs in particular, the cost incurred is almost two times the income they earn from their BC business, whereas the urban CSPs seem to fare much better, with commissions exceeding expenditures by a fair margin. Data reveals revenue from the money transfer (remittances) is the main driver of the overall revenue earned by the urban CSPs. Therefore, more useful products should serve through the CSPs in the rural areas to make the BC model feasible. Further, it might offer more efficient incentive for rural CSPs that could ensure break-even in their business.

Challenges in managing cash: CSPs face a multitude of problems, of which, the most prominent are cash management and liquidity issues. One reason for this is inadequate sharing of cost and risks associated with cash management among principal bank, BC and CSPs, leaving CSPs to bear extensive risks on their own. Crisis in the cash management arises due to a variety of circumstances. Firstly, issues of cash deficit or excess are experienced in locations that witness significantly more deposits over withdrawals or vice versa. This problem is compounded by a mandatory limit imposed on cash balances at the CSP (balance/transaction limits in a day), which might be a good policy but often put CSPs in a difficult situation. Especially CSPs in rural area face a huge cash shortage as demand of withdrawal of remittance money and government payments are high.

In view of these difficulties, the principal bank could allow CSPs (on merits) to access overdraft facilities at minimal cost for a shorter time period. This would go some way towards helping CSPs resolve the aforementioned cash management issues. Further a greater clarity should be established with regards to the cost sharing for cash management and associated risks.

Need of Product diversity: The BC channel has been extensively used to offer ‘no-frills’ account, with the perception that the targeted clientele hardly need any other financial products. However, the study shows most clients demand a wider set of financial products and services such as more savings options (8%), government payments (12%), value added services (22%) and a large section of clientele (74%) demands loan facilities too. 31% of CSPs surveyed also echoed the need of wider set of products in an equal direction as client expressed their desire during the survey. RBI should proactively provide some direction in regard to catering diverse set of client centric financial services and products through this channel.

Furthermore, the study highlights discrepancies between the facilities and scope of ‘no-frills’ accounts across banks – some banks provide debit cards, passbooks and a cheque book to clients whereas others have certain restrictions on these facilities. In addition, the scope of NFAs is too narrow which has cap on maximum balance and limited numbers of transactions (deposit) in a month etc. and it does not fulfil the diverse needs of clients. Uniformity is essential in offering services and facilities through services and RBI need to examine the concept of ‘no-frills.’ It could be converted as basic saving account as the nomenclature has become a stigma and the scope of this savings product is not fulfilling the clients’ need.

Promotion and marketing: While the BC channel is considered to be a promising model for promoting financial inclusion, surprisingly little effort has been put forward to promote the model and its benefits among prospective clientele. Neither banks, BCs nor CSPs are willing to invest in promoting the model, its products and services. For instance there have only been a few recorded cases of banks and BCs organizing marketing campaigns and, even then, only doing so at the launch of the facility. Thereafter, there was essentially no engagement by either the banks or the BCs in building awareness amongst the clientele. The RBI and principal banks should engage and invest time and effort in promoting the BC model and its benefits. The RBI should also place greater effort and emphasis on building acceptance of the BC model amongst prospective stakeholders, including clients.

Efficiency in client selection and educating client about the model:

The study revealed that large sections of BC clients (61%) are, at the same time, ‘regular savings-bank account’ holders. It suggests that the client selection processes under the current BC arrangement are not efficient enough to target right clientele. As a result, we are far from meeting the broader objectives of BC initiative those intend to extend banking services to the financially excluded household. This could be due to the lack of assessment criteria for client selection and if there is an existing criterion, this criterion is clearly not being followed. The RBI along with other key stakeholders should take this concern seriously and consider formulating better guidelines to improve the efficacy and efficiency of the client selection process to expand outreach to financially excluded section of the population.

Further, the study reveals that there is a dearth of financial literacy amongst clients regarding the usability of NFAs. There have even been cases where, due to lack of awareness about the account and its usability, clients are unable to get benefits of it in terms of accessing government payments, insurance reimbursement etc. At the same time, clients are also largely unaware of transaction limitations placed on NFAs that disallow them from accepting large deposits such as Indira Awaas payment etc. Therefore, a certain level of financial literacy education amongst clients is essential to the success of the BC model. The Government, RBI and principal banks can spearhead this movement through the planning and implementation of dedicated campaigns.

Client Satisfaction: Significantly large section of clients (85%) surveyed reported being satisfied with the services and behaviour of their CSPs and BCs. On top of that, about 90% of clients said that they find it easier and safe to do transactions with agents as compared to banks and other sources. This clearly indicates that the targeted clientele accepted the BC model.

This model of banking has the potential to take the financial inclusion drive to further heights. However, RBI and government should ensure effective functioning of the BC model by offering wider range of client-centric financial products and services with an emphasis on financial education of clients’ as well. Also, RBI should provide clear guidance in safeguarding business prospect of this model of banking that could leads to financial viability of the stakeholders at every level.