Helping the poor save more towards a specific goal, could be as simple as providing them a safe, secure device for savings – something as simple as a Piggy Bank or a Safe Box. Sounds too simple?

Based on a RCT conducted by Dupas and Robinson (2012) in Western Kenya, providing the poor a Safe Box increased informal savings for health services by as much as 66%, compared to the comparison group. The experiment took place in Western Kenya with 113 ROSCA (Rotating Savings and Credit Association – where a group of individuals meet for a set period of time to save and borrow) participants, who were randomly assigned to treatment or control.

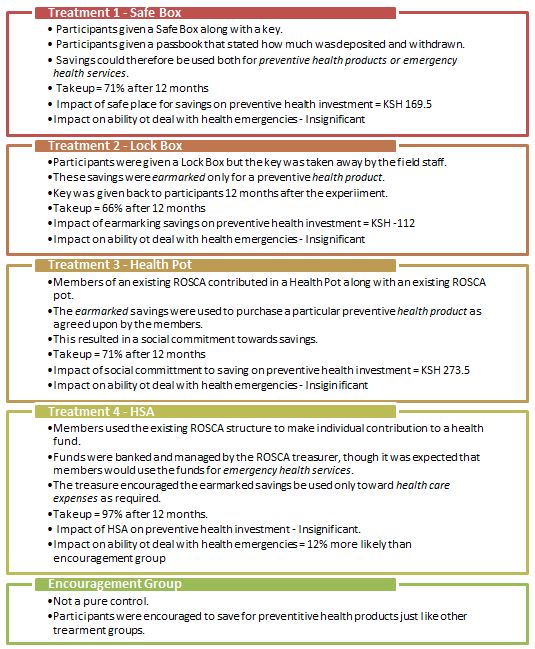

4 treatment groups were set up along with 1 control group, and all these groups were encouraged to increase savings for particular health products such as bednets, water filters, and water chlorination; therefore the differences seen could be attributed to the different saving technologies. Randomization was done after stratification on characteristics including gender composition in ROSCA, meeting frequency or ROSCA and whether ROSCA provided loans. The impact of the following 4 savings technologies was measured on (1) take-up of the various savings technologies; (2) investments in preventive health products; and (3) whether household are able to deal with emergencies when they arise.

The study found that:

- A safe storage device has impact – Merely having a health savings storage device helps “shifting the reference consumption basket towards health goals”. Mentally labeling savings towards a particular goal, helps people save towards that goal, and it makes those funds less fungible and less susceptible to demands from friends and relatives.

- Providing credit along with the social pressure to save for a health goal in group settings increases investments and in this case, preventive health investments.

- People prefer earmarking for medical emergencies than preventive health and because earmarking has a liquidity cost associated with it, medical emergencies are held more valuable than preventive health.

However, there are interesting exceptions that arise; those taxed by their social network (people who give assistance to others but receive none in return) are the only group that continued to save for deposits earmarked for preventive healthcare, therefore earmarking these savings must outweigh the liquidity cost of keeping those savings locked away for preventive healthcare use. The savings may have the potential to the reduce pressure of sharing the money at home, therefore helping respondents exerting self-control. Secondly, people with the “present-bias” (time inconsistent behavior – http://en.wikipedia.org/wiki/Dynamic_inconsistency) didn’t gain from the safe box or lockbox (Treatment 1 and 2) because of temptation and lack of self-control. They did benefit social commitment devices (Treatment 3) because of the social pressures to save. Lastly, having a secure place for savings might be a very valuable exercise for people who are over-coming household barriers to saving within a household.

There are limitations to the study though – the respondents were already using the ROSCA structure, and were more educated and from a higher income demographic compared to the larger population. In addition, since they self-selected into the ROSCA, they had a higher propensity to save. Therefore, it is difficult to extrapolate the findings to the general public trying to figure out a way to save. Additionally, an important observation must be made about the premise of this study, as it was based on the assumptions that the (1) poor don’t save enough because of temptation spending which negatively affects them more than the rich, (2) limited attention span leads to insufficient focus on savings, (3) there need to be interventions such as text message reminders or peer group support to increase savings products. While these assumptions are valid, they are also patronizing suggesting that poor need more hand-holding and discipline compared to those who are well off. However, behavioral economists Bertrand, Mullainathan, and Shafir (2006) suggest that the poor make decisions just like the rest of us, but other important factors impact their savings decisions – (1) poor are treated differently than those that are well off, which makes them less likely to seek financial advice and products, (2) transaction costs of operating bank accounts and using bank services is higher for poor than the rich, (3) most financial services are geared towards the financially able people, and do not directly target the financially excluded sector.

The researchers in this study overcome some of these barriers, (1) the savings technology is relatively easy to use and is not attached with any social stigma resulting in a low take-up, (2) there are no apparent reasons why participants should discriminate against each other, making this form of savings more inviting, (3) the transaction costs to using these savings technologies is relatively low.

While the research analyzes the use of simple tec

hnologies to increase savings, it might also be interesting to determine what these savings are used for and whether the respondents were merely displacing their savings from ROSCA. It may also be interesting to replicate the study in low-income areas where the concept of group savings does not exist and where the culture of savings is not common, because these are areas where savings can have a large impact of people’s economic welfare.

hnologies to increase savings, it might also be interesting to determine what these savings are used for and whether the respondents were merely displacing their savings from ROSCA. It may also be interesting to replicate the study in low-income areas where the concept of group savings does not exist and where the culture of savings is not common, because these are areas where savings can have a large impact of people’s economic welfare.